What Can Home Buyers Learn To Navigate Market Turbulence?

Author: Kevin Graham

The housing market is at the tail end of another home buying season. Since the pandemic, the real estate market is experiencing a fair amount of volatility.

An early freeze on home sales in March and April 2020 quickly gave way to the hottest market in recent memory as Americans looked for new spaces to fit their current lifestyle, a frenzy supported by low rates. As hot as the market conditions were through the end of 2021, it caused affordability issues.

The Federal Reserve has since made moves to get inflation under control that have caused interest rates to rise across the board. The problem? Home prices haven’t come down. Not only do home prices tend to be sticky, but inventory remains very low. The issue is most visible for existing homes, which make up the majority of overall sales.

If current homeowners were plucked out of the sky and dropped into the housing market right now, they might find it very challenging, particularly as a first-time home buyer. Still, it can be easy to fall into recency bias. How do the expectations and challenges of today’s first-time home buyers compare with those of previous generations?

Just as important as picking things up from current homeowners are the strategies that buyers can use to navigate today’s market turbulence. We’ll highlight a creative down payment program that can help.

Rocket Mortgage® surveyed 1,500 people on a variety of topics with the goal of uncovering the answer to that question. The survey group consisted of a mix of current homeowners and those who are currently in the market for their first home.

Rising Home Prices Are Creating A Down Payment Obstacle For Current Home Buyers

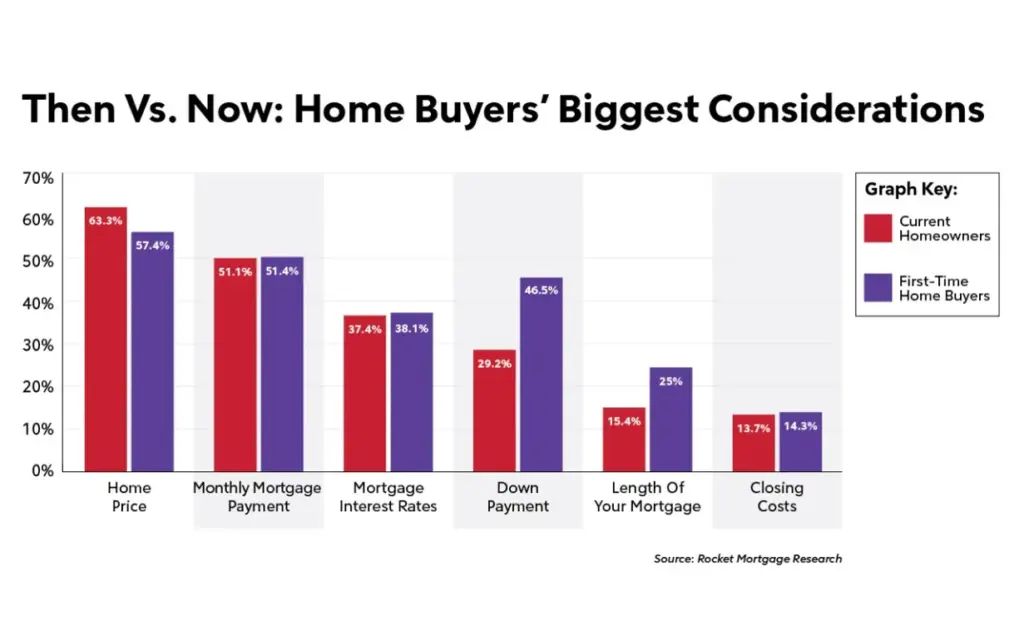

Any analysis of generational differences among first-time home buyers should probably begin with the items that were most important to them when they were looking for their first home.

Let’s start by looking at the top three concerns of current homeowners. The number in parentheses indicates the percentage of respondents for whom this was a concern:

- Home price (63.3%)

- Monthly mortgage payment (51.1%)

- Mortgage interest rates (37.4%)

When it comes to first-time home buyers, it’s much of the same at the top with one difference.

- Home price (57.4%)

- Monthly mortgage payment (51.4%)

- Down payment (46.5%)

The down payment concern likely has to do with home prices rising rapidly and first-time home buyers not feeling like they have enough saved to put a significant amount down on a home. That’s certainly an understandable concern, but it doesn’t have to be an obstacle that can’t be conquered. Although there are certain advantages to a higher down payment, such as avoiding private mortgage insurance on a conventional loan, most first-time home buyers only have to put 3% – 3.5% down.

Later in the article, we’ll discuss several alternatives, including ONE+ from Rocket Pro TPO, which allows you to put 1% down with a 2% lender grant.1 This might mean allocation of funds for other items.

It’s interesting to note that first-time home buyers are feeling the effects of the double whammy of higher home prices and elevated mortgage interest rates. While mortgage interest rates were outside the top three considerations among this cohort of first-time buyers, more of them rated it as a significant concern than current homeowners (38.1% vs. 37.4%). Let’s go a bit deeper on that.

Interest Rates Were Less Of A Concern For Home Buyers Pre-2020, Even At Their Highest

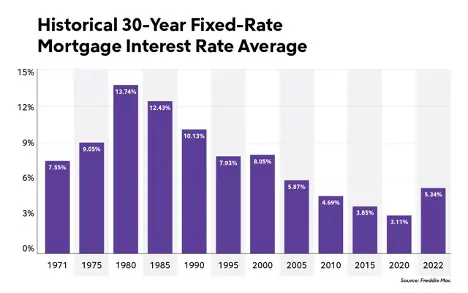

It’s also illuminating to see that certain things matter more to first-time home buyers today than they did in the past. As a top example, more home buyers who bought in the 2020s considered mortgage rates their biggest concern than anyone in the 80s, 90s or 2000s.

45.7% of home buyers in the 2020s said mortgage rates were their biggest purchase consideration. Those who have studied 1980s interest rates may be familiar with the fact that they were sky-high. The average rate according to the Freddie Mac Primary Mortgage Market Survey® got as high as 16.63% in 1981.

What’s really interesting here is that outside of a brief upward blip in 2016 just before Brexit sent rates tumbling again, most people who bought homes in the last decade leading up to last year got used to interest rates that were abnormally low in the broader context of history. For rates to suddenly be going up as this group is looking to buy seems to be a shock.

Furthermore, term length was a bigger concern in the 1980s – 2000s than it was in the teens and 20s. Here are the percentages from each decade of people who rated their highest concern as how long they spent paying on the mortgage.

- 1980s: 26.5%

- 1990s: 25%

- 2000s: 17.4%

A significantly higher proportion of homeowners felt that down payment was the biggest concern in the 2010s and 2020s compared to homeowners who bought in the 70s through 90s, possibly owing to higher home prices (more on that later).

- 2010s: 29.5%

- 2020s: 35.8%

First-Time Home Buyers Are Struggling With Housing Prices

There’s no doubt it’s a hard market out there for those looking to buy. Patience is key because inventory is limited. Rely on the guidance of a real estate agent as well. But what are home buyers up against in this market compared to others?

People don’t have perfect memories, but we did want to get their sense of what they felt they paid and the mortgage rate when they bought. This was compared to historical records for mortgage rates and home prices.

It’s worth noting that while the majority of home sales in the U.S. are already existing homes, new home sales data is easier to come by over a longer period. That data is from the Department of Housing and Urban Development as well as the Census Bureau. The mortgage rates referenced are from the Freddie Mac Primary Mortgage Market Survey. The average mortgage rate is based on the average of the reported weekly data for each year listed. The home price data in the graph is the average of the median home prices for each quarter in the reported year.

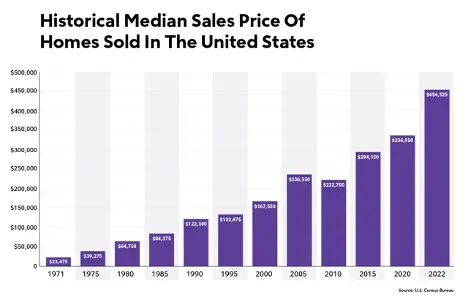

In the 2000s, home prices start rising incredibly quickly. The average home price at the beginning of the decade was $167,550 and ended at $222,700. The average purchase price for the surveyed first-time home buyers during this decade was steady at $100,000 – $150,000. This was when 21.1% of the surveyed current homeowner population bought their first home. The average interest rate was 8.05% to begin the decade and 4.69% by its end.

The late 2010s began a long period of falling interest rates, touched off by the financial crisis. While they started in the low 5% range, the average fell to 3.11% in 2020. The biggest cohort of current homeowners bought their first home during this time, 36.6%. These low interest rates supported a huge run-up in home prices. Those queried who purchased in this window did so for $150,000 – $200,000, while the average price according to the Census Bureau over this time period was $222,700 to begin the decade and $336,950 to end it.

The 2020s have seen several interest rate fluctuations. The pandemic ushered in a time when declines meant they were at rock bottom for a while, but the Federal Reserve has since moved to pull back on some of its accommodative policy to bring inflation under control and also give it a chance to go lower with rates in response to downturns.

While the average interest rate to begin the decade was in the high 3% range, more recently it’s gotten as high as 7.08% for the 30-year fixed in late October and early November of last year. As of this writing, it’s even topped that, touching 7.31% for the week of September 28, 2023. Yet, in many ways, prices are behaving as if it's still a low-rate environment. The current homeowners who bought their home during this decade have budgeted between $200,000 – $250,000.

But the average price of the new home at this time has gone from $329,000 to $467,700 in a few short years. This has forced first-time buyers to reevaluate their budgets. And they are budgeting anywhere between $200,000 – $350,000 on average.

Because inventories haven’t kept up with the number of homes that are in demand, these home buyers have typically been searching for 5 to 6 months. Of those surveyed, 45.2% have found the search process difficult, 21.4% see it as easy and the remainder are neutral. Of those who find it difficult, the biggest factor causing distress for 81.9% of them is the price.

Beyond price dynamics themselves, one of the hardest pills to swallow is the number of homes that are selling over asking price. According to the latest available data from Rocket HomesSM for July 2023, 35.6% of homes were selling over the asking price.2 In many cases, the offers that people are getting are coming in higher than the appraisal.

Because a mortgage lender can only do the loan based on what an independent appraiser values the home at, people are forced to bring the difference between the appraised value and the agreed-upon purchase price to the closing table. First-time home buyers in particular may have a hard time coming up with this in addition to the minimum down payment and other closing costs with today’s inflationary economic conditions. The good news here is there are signs of change. This is how buyers can react to this market.

Action Items For First-Time Home Buyers

With so many homes going for above asking, what’s the recourse for a first-time home buyer with limited resources? One key could be finding a loan option with a lower required down payment. Buyers can use funds that would normally be put toward a down payment to bring the gap between the appraised value and accepted offer to the table.

ONE+ is a conventional mortgage option where buyers can put 1% down and receive a 2% grant toward their down payment from Rocket Pro TPO. Borrowers have the option of putting down up to 3% and still receiving the grant.

Moreover, there is no borrower-paid mortgage insurance with this loan option. On a $250,000 loan amount, that’s a savings of up to $245 per month. Because it takes an average of 7 years for clients to reach 20% equity and qualify for mortgage insurance removal, that equates to $20,500 in savings over that time frame.

Of course, buyers do have to qualify for this option. Here are some key things to remember:

- Your client can’t make more than 80% of the median income where they’re looking to buy. If they’re looking in Birmingham, Alabama, the area median income is $89,600. Their qualifying income can’t be higher than $71,680 ($89,600 × 0.8 = $71,680). Fannie Mae has a tool that allows you to look up their area median income.

- Your client needs a qualifying FICO® Score of 620 or better.

- Your client has to be purchasing a 1-unit primary residence.

- Your client’s total down payment with the grant can’t be more than 5%.

It’s important to note that when we talk about income limits, that’s qualifying income. If your client is on the edge of qualification and they can afford their home without counting bonus or commission income, that doesn’t need to be included. This option is available for both first-time and repeat home buyers.

Those who qualify can qualify with as little as 3% down. Whether a first-time home buyer or buying their tenth home, the highest minimum down payment for a 1-unit primary residence on any product is 5%.

The ability to make a lower down payment could enable your client to make a competitive offer even if appraised values aren’t keeping up with the bidding wars going on in hot markets by allowing them to make up the difference.

The other thing to remember is that, despite national numbers being widely reported, the housing market can vary from neighborhood to neighborhood. So it’s really important to have a real estate agent who can advise on leverage. For example, a buyer could have more room to negotiate if the house has been on the market a while.

If the home has been hanging on the market, the seller may be more willing to negotiate on price. Alternatively, maybe the price doesn’t move, but they offer some seller concessions to help with closing costs.

It’s also not just about price, but about the cost of the mortgage payment for some. One of the ways to potentially save on interest is getting the seller to contribute to mortgage points to permanently buy down the rate. If that’s not in the cards, there are also temporary buydowns to pay a lower rate for the first year or two of the mortgage.

The last thing the seller could help with if they won’t budge on price are repairs to the home that may be necessary either before or shortly after moving in. This may be an especially useful tactic if the seller is motivated to move or there are any deal breakers that came up in the home inspection.

Bottom Line

There’s no doubt that home buyer concerns have expanded compared to the past. Price, mortgage payment and interest rate have always been a concern, but now prices have gotten so high that buyers are concerned about affording a down payment. And while location remains a primary concern, its importance is lessening in the minds of many home buyers.

People who were in the market when rates were lower and decided to hold off are also struggling with the idea of interest rates being as high as they are. However, there are options. Buyers can look at buydowns, particularly if they have a seller or real estate agent who’s going to negotiate on concessions or a piece of their commission to fund it.

One of the primary concerns for buyers is that home prices have remained fairly high despite interest rates rising. While no one can control the invisible hand of the market and bring prices down, having a lower down payment can help your clients with having money to bring to the closing table when there’s a gap between the offer and the appraisal. ONE+ could be a good option. It allows qualified home buyers to put 1% down while receiving a 2% grant from Rocket Pro TPO. First-time home buyers not meeting those income limits can still get into a home with as little as 3% down.

Methodology

In order to understand the difference in what was impacting current homeowner’s and what is impacting current home buyer’s ability to purchase, Rocket Mortgage surveyed 1,500 American adults 23 years old and older. Respondents were split between 62% that are current homeowners, and the other 38% being current first-time home buyers. Respondents from both groups were asked about their biggest considerations in the home buying process, wish list items for a home, and other general home buying questions and concerns. This survey was conducted February 8, 2023.

1Client will be required to pay a 1% down payment, with the ability to pay a maximum of 3%, and Rocket Mortgage will cover an additional 2% of the client’s purchase price as a down payment. This offer is only available on conventional purchase loans. Primary residence only. Cost of mortgage insurance premium not passed through to client. Offer valid only for home buyers when qualifying income is less than or equal to 80% area median income based on county where property is located. Must lock rate on or after 5/22/2023. Not available with any other discounts or promotions. Offer cannot be retroactively applied to previously closed loans or loans that have a locked rate. This is not a commitment to lend. Rocket Mortgage reserves the right to cancel this offer at any time. Acceptance of this offer constitutes the acceptance of these terms and conditions, which are subject to change at the sole discretion of Rocket Mortgage. Additional restrictions/conditions may apply.

This article was originally posted on RocketMortgage.com and has been edited for our partner audience.